If you’ve had even half an eye on the news recently, you may have seen the discussions around the future of the “triple lock”. This is a government pledge to ensure that retirement income from the State Pension rises in line with inflation.

If you’ve had even half an eye on the news recently, you may have seen the discussions around the future of the “triple lock”. This is a government pledge to ensure that retirement income from the State Pension rises in line with inflation.

However, one impact of the pandemic is that the triple lock calculation could mean a substantial increase in the State Pension, which will create big problems for the chancellor as he tries to steer the economy back on track.

In this article we’ll look at the triple lock, why it’s important, and how the proposed changes could impact on you.

The triple lock is a pledge to ensure the State Pension keeps track with rising inflation

In his 2010 budget, the then-chancellor of the Exchequer, George Osborne, introduced the triple lock. The aim was to ensure that the State Pension kept up with increasing prices, rather than be subject to political pressure each year.

As the name suggests, the criteria involve three different figures. Each year, the State Pension increases by the highest of:

- The rate of inflation using the consumer price index (CPI) measure

- The increase in national average wages

- 2.5%

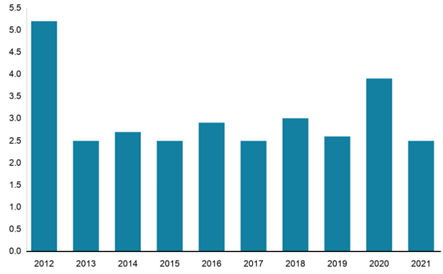

As you can see from the table below, after an initial increase of 5.2% in April 2012, subsequent increases have averaged around 3% a year.

Source: BBC

High unemployment during the pandemic has skewed average wage figures

In November 2020, the government announced that the triple lock would ensure the State Pension went up by 2.5% the following April. However, at that time, we were in the midst of the pandemic and millions of people were laid off or on furlough, meaning that the wage increase figure was very low.

Looking ahead to November 2021, when the government will be expected to make a similar announcement, the pandemic means different factors come into play.

As the economy starts to re-open, wages have increased rapidly and many experts, including the Bank of England, have predicted that the wage increase figure could be as high as 8%.

Based on the triple lock criteria, this would mean the State Pension goes up by a corresponding amount. This will increase the State Pension from £9,339 in the 2021/22 tax year to £10,086 in the 2022/23 tax year.

An 8% increase in the State Pension could require a tax increase

One of the problems with this is that, while an 8% increase would be valuable to retired people, it could pose a problem for the government. The Treasury would have to find the money for the increase this year, and then further increases on top of that each year going forward.

Understandably, there are strong differences of opinion over what the government should do.

If the 8% rise goes ahead, it would leave a significant hole in the Treasury that would probably need to be filled through an increase in taxes. At a time when many households are struggling to keep their heads above water, due to the economic impact of the pandemic, this may not be wise.

However, some campaigners and members of the opposition parties believe that the government should honour the pledged increase. They point to the fact that the UK State Pension is relatively low compared with other European countries.

Age UK have also previously expressed concern at the government’s own figures, which show 200,000 more pensioners in poverty this year compared to 2020.

There’s also a very strong political, and electoral, dimension to the current debate.

According to MORI, 64% of people over 65 voted Conservative in 2019. In a similar survey in 2010, the election before the government implemented the triple lock, the figure was 44%. That’s a sizable increase in a very short period, and it’s highly likely that the triple lock has contributed to this dramatic rise in support.

The government is divided over whether to go back on their triple lock pledge

While the government may want to avoid the expense of the State Pension rise, they also need to consider how unpopular scrapping the triple lock would be. Essentially, they have four main options:

Accept the pension rise

The government’s first option would be to simply bite the bullet and accept the rise mandated by the triple lock pledge. This would probably make pensioners very happy but not the Treasury, given how expensive it would be to honour it.

Change the criteria for this year on a one-off basis

The second option that the government has is to cite “extenuating circumstances” for this year and average the increase over the last two years instead. This would work out at a respectable increase of around 5.25%.

Change the criteria for calculating the State Pension

One of the more moderate proposals is to remove wages from the calculation and create a “double lock” pledge instead, based on the highest of a flat annual increase or the rate of inflation.

Abolish the triple lock pledge

The final option that the government has is to scrap the triple lock and return to the old system whereby the State Pension increases were dictated by the chancellor. However, while this might save the government money, it could be very unpopular with the electorate.

Unfortunately for pensioners, there are signs that the chancellor may not be willing to implement the proposed 8% increase. In an interview with the BBC, he was quoted as saying that the decision should be based on “fairness for pensioners and for taxpayers”.

How changes to the triple lock could impact on you

If you’ve already retired, the removal of the triple lock probably won’t have a massive impact. Previous increases to the State Pension will be maintained, and it’s almost certain that some kind of pledge increase will remain in place, such as the previously mentioned double lock, to ensure your pension continues to keep pace with rising prices.

However, the impact could be more severe if you are not yet drawing your State Pension and are still working.

The State Pension is probably not enough to live comfortably on, and it’s sensible not to rely on it too much when it comes to planning for your retirement. Instead, you may want to consider it as the bedrock of your finances in retirement, topped up by your private pensions.

If you want to reduce any uncertainty over your finances in retirement, one of the best things you can do is to increase your pension contributions while you can, to reduce your reliance on the State Pension.

Get in touch

If you want to know more about how the proposed changes to the triple lock could affect you, get in touch. Please email info@investmentsense.co.uk or call 0115 933 8433.