Pensions Freedom – A summary of the key changes

In 2015 the retirement rules were rewritten, we will therefore start with a summary of the main changes.

The rules, which came into effect from April 2015, changed the way people take money out of their pensions, with new freedoms and options available to anyone over the age of 55.

In this part of the guide we explain the key changes, how they could benefit you and some of the pitfalls to look out for.

Change #1: Unrestricted access to your pension from 55

Prior to the new rules taking effect, the maximum amount available to be taken from a pension each year was capped; this is no longer the case.

Anyone over the age of 55 now has complete access to their pension, with no limit to the maximum lump sums or income available. In reality, this means people generally take one of four options:

- Take the whole pension pot as one lump sum; 25% will be tax-free with the remainder added to your income and potentially taxed at 20%, 40% or 45%

- Take smaller lump sums as and when needed; as above, 25% will be tax-free, the remainder will be added to your income and potentially taxed at 20%, 40% or 45%

- Take up to 25% of the fund as a tax-fee lump sum and defer taking an income until a later date

- Take up to 25% of the fund as a tax-free lump with the balance used to provide a regular income using an Annuity or Flexi-Access Drawdown (the new name for Income Drawdown)

Anyone considering taking lump sums above the 25% tax-free amount, must be careful not to fall into the trap of miscalculating the tax they should pay. For example, a basic rate taxpayer might assume any additional lump sum will simply be taxed at a rate of 20%. This could be the case. However, if the lump sum, when added to their other income in the tax-year in question, takes you into higher rate tax, you could end up paying 40% on some or all the amount you withdraw, leaving you with less than you anticipated.

There are ways of minimising the tax you pay on lump sum withdrawals, for example staggering the lump sums over multiple tax years. Alternatively, you could wait to withdraw lump sums until tax years when your income is lower, for example after you have retired.

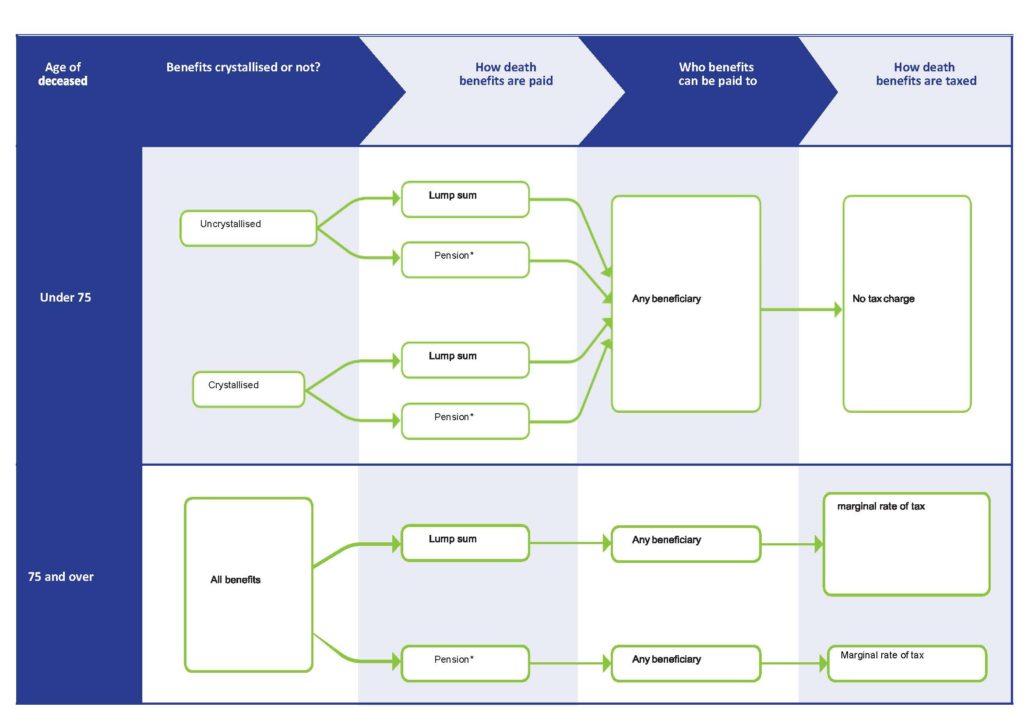

Change #2: Lower taxes on death

The new rules mean that the tax paid by your beneficiaries from lump sums from drawdown arrangements is dependent on when you die and can be summarised as follows:

Change #3: Pensions Wise

As part of the changes, anyone over the age of 55 is able to get free guidance and information on the options available to them.

The service is called Pensions Wise and is run by The Pensions Regulator in conjunction with the Citizens Advice Bureau.

Pensions Wise can offer you guidance about the options available to you. According to its website it is: “A free and impartial government service that helps you understand your pension options.”

However, “Pension Wise won’t recommend any products or tell you what to do with your money.”

At present the service is only available to anyone over the age of 55. During your appointment with Pensions Wise you will discuss:

- The various ways you can take money from your pension pot

- The implications of each option for your circumstances

- The various next steps you could take

It is important to emphasise that the service provided by Pensions Wise is very different to, and does not replace, an Independent Financial Adviser.

Pensions Wise will not recommend products, companies or specific investments; only a regulated financial adviser can do that for you. Furthermore, Pensions Wise does not provide an ongoing service, which many advisers do.

The best way to compare the two is to think of guidance as providing high level information, after finding out a little about your circumstances. In contrast, advice is a full recommendation, only made after a fact-finding process, which will include a recommendation as to which product, provider or investment is most suitable for your needs.

Indeed, many people believe that once guidance has been given by Pensions Wise, a referral to a financial adviser will be necessary so that specific advice and technical assistance can be given.

Change #4: Transferring Final Salary and Defined Benefit schemes

Members of Defined Benefit and Final Salary pensions are able to take advantage of the rules if they transfer away from their current scheme into a personal arrangement (e.g. Personal Pension, Stakeholder Pension or Self-Invested Personal Pension).

However, to make such a transfer, if the value of your benefits exceeds £30,000, you must have taken independent advice and some schemes, such as public-sector pensions, no longer allow a transfer to take place.

Before transferring away from a Defined Benefit or Final Salary pension it is vital you consider the disadvantages of doing so and take independent financial advice.

In most circumstances making such a transfer will not be in your best interests.

Change #5: Tax cut on widow’s / widower’s pensions from an Annuity

Many people choose to include a widow’s or widower’s pension when they buy an Annuity, to ensure their spouse is financially secure in the future.

Under the old rules, the spouse’s pension would be added to the existing income of the widow or widower and taxed accordingly at their highest marginal rate of income tax. Furthermore, it was only possible to include a pension on your death for your spouse, civil partner or other financial dependent.

Under the new rules, if you die before the age of 75 and have a Lifetime Annuity, your spouse will receive their widow or widower’s pension tax-free.

The rules on who can receive the income when you die, have also been relaxed, and are no longer restricted as was previously the case.

Ask a financial planner

Whatever your question, our team of financial planners are here to help. Alternatively, if you’d like to book a no-obligation meeting or call, we’d be happy to arrange a suitable time.

Simply complete this form and we’ll get straight back to you.