When times are tough, it’s usually a good idea to hold some of your wealth in cash as a financial cushion. However, problems can arise if you hold too much of your money in this way.

When times are tough, it’s usually a good idea to hold some of your wealth in cash as a financial cushion. However, problems can arise if you hold too much of your money in this way.

While sitting on a large stockpile of cash can make you feel more financially secure, in the long term this could have negative consequences for your financial wellbeing. Read on to find out the pros and cons of holding too much of your wealth in cash.

Keeping an emergency fund can help you absorb financial shocks

As you may have read about in a previous article, it’s important to keep an emergency fund if you’re financially insecure, as it can help protect you against unexpected disruptions. This can be particularly true for younger people, who tend to be more financially vulnerable and so may have to rely on expensive credit to absorb financial shocks.

For example, if you were made redundant, having an emergency fund in place could cover your expenses until you got back on your feet.

With this in mind, most experts typically recommend that you keep enough money in your fund to cover three to six months’ worth of expenses. This can give you some breathing room while you recover.

However, if you are self-employed or you work in a field which is particularly at risk during a financial downturn, then you may want to consider keeping a larger fund.

While this is a sensible precaution, it can be easy to fall into the trap of holding too much of your wealth in cash. Even though this will give you a larger financial cushion if the worst were to happen, you may find that low interest rates eat away at the true value of your wealth.

Low interest rates can make holding cash a poor long-term prospect

One of the biggest problems with holding your wealth in cash is that many banks are currently offering low interest rates. Due to the economic impact of the pandemic, the current Bank of England base rate is just 0.1%.

This means that if you hold your wealth in cash, it is unlikely to grow by a meaningful amount over time. This can pose a problem for savers if the rate of inflation is higher than the rate of interest on your savings.

If this happens, then the true value of your cash will be eroded as the interest does not keep pace with the increases in the price of goods. This would mean that your spending power could fall significantly.

You can use the Bank of England’s inflation calculator to see the effects of this over the long term.

For example, if you had £20,000 worth of savings in your emergency fund in 2010, for it to have the same spending power in 2020 you’d need your savings to have grown by £6,225, as inflation averaged at 2.7% throughout that period.

If you want to be sure to meet your financial goals, it’s important to use your wealth effectively but keeping too much of it in cash can impair its ability to grow.

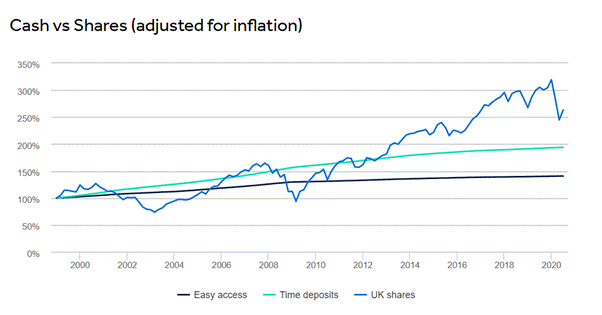

As you can see from the graph below, investing your wealth rather than keeping it in cash can mean that you could get a much better return.

If you held £100 in cash from 1 January 1999 until 30 June 2020 then it would have grown to £198, or £124 after inflation. On the other hand, if you had invested for the same period, it would have grown to an impressive £432, or £284 after inflation.

It should be noted however that Equity investments do not afford the same capital security as deposit accounts. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Source: Hargreaves Lansdown

Having financial protection can negate the need for a large emergency fund

While it’s understandable that you may want to keep a sizeable portion of your wealth in cash during a period of financial instability, this may not be the most effective way to use your wealth.

Instead of keeping a larger emergency fund, a more sensible alternative might be to put financial protection in place, which can help you to overcome disruptions without the need for a large cash reserve.

Not only can protection help to ensure that your progress towards financial goals isn’t disrupted by shocks, but it can also give you invaluable peace of mind.

Some of the most common examples of financial protection are:

Income protection

If you’re unable to work due to accident or illness, income protection will pay you a portion of your monthly salary while you get back on your feet. These payments typically last until you recover or until the end of the policy term.

While this form of protection usually covers most illnesses that leave you unable to work, you should check the terms of the policy thoroughly to see what you are protected against.

Critical illness cover

If you are diagnosed with a serious illness, it can be emotionally and financially difficult. If you are unable to work because of it, you may need to dip into your savings to pay for treatment and this can add to your stress.

Critical illness cover will pay you a lump sum if you are diagnosed with a serious illness. You can use this money to pay for private medical care, repay your mortgage, or maintain your standard of living if you need to take prolonged leave from work.

Having financial protection in place can mean that you don’t need such a large emergency fund, allowing you to grow your wealth effectively while still knowing that you’ll be able to overcome any unexpected disruptions.

However, please bear in mind that life assurance plans typically have no cash in value at any time and that cover will cease at the end of the term. Furthermore, if you stop paying premiums, your cover will lapse.

Get in touch

If you want to protect your financial wellbeing while growing your wealth in the most effective way, get in touch. Please email info@investmentsense.co.uk or call 0115 933 8433.

Please note:

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.