If you’ve been following the news at all in recent months, you may have noticed that the term “wealth tax” is appearing more frequently.

If you’ve been following the news at all in recent months, you may have noticed that the term “wealth tax” is appearing more frequently.

While this isn’t a new idea in the UK, this increased commentary could suggest that it might soon become more than just a talking point.

The upcoming Autumn Budget – which is expected in late October or early November 2025 – could introduce new significant financial legislation as the chancellor, Rachel Reeves, looks for ways to balance the country’s finances.

A wealth tax is one such measure that the chancellor could announce. According to YouGov, 75% of British adults would support the move.

Yet, the Institute for Fiscal Studies states that a wealth tax would be a “poor substitute for properly taxing the sources and uses of wealth”, and that it would be incredibly difficult to set up.

At this stage, it’s vital to note that no announcements have been officially made, and introducing a wealth tax is still just speculation.

Still, if you’ve accumulated considerable wealth, you might be wondering what a wealth tax might involve. Continue reading to find out how it might affect your finances.

A wealth tax would involve taxing your existing wealth instead of your income

A wealth tax is essentially a levy based on the total value of your assets, rather than just your income.

Indeed, unlike Income Tax or National Insurance, it would target your accumulated assets, such as property or investments.

It could either apply as a one-time charge, or occur each year, depending on how it’s structured.

One proposal that has been mentioned is a 2% annual tax on net assets over £10 million. Meanwhile, others have floated the idea of a 1% charge for those with more than £4 million.

MoneyWeek reveals that a tax of this kind could raise £25 billion for the government each year.

Other alternatives to a wealth tax have been suggested, too. In 2014, the Labour Party promoted a “mansion tax”, targeting properties valued above £2 million. While the idea never became a law, it might still influence the party’s policies today.

Rather than introducing an entirely new tax, the government may simply decide to reform existing ones.

For instance, they could adjust Council Tax to introduce more bands at the top end, which would increase the charge on high-value homes.

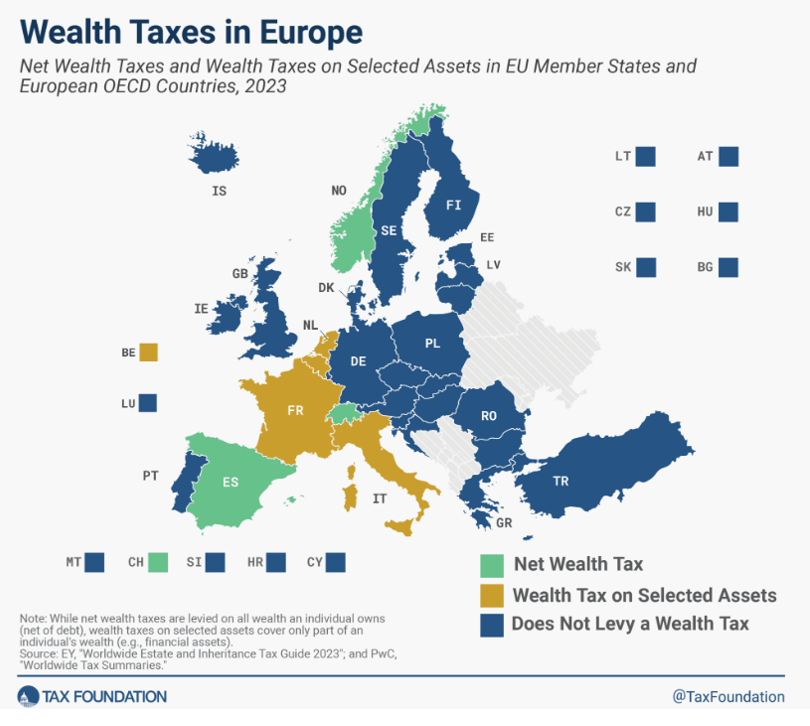

Several countries have already introduced a wealth tax with varying degrees of success

It’s worth noting that several countries around the world have already implemented some version of a wealth tax.

In South America, Chile has imposed a 2% annual tax on specific high-value items, such as luxury cars, yachts, and helicopters.

Meanwhile, Colombia has approved a permanent wealth tax on people with a net worth exceeding $642,000. Then, they will be taxed between 0.5% and 1%, although a higher rate of 1.5% will apply until 2026.

The rules vary significantly in Europe, as the map below shows.

Source: The Tax Foundation

Spain has introduced a temporary “solidarity tax” on residents with more than €3 million in assets, effective during 2022 and 2023.

France also applies a wealth tax to global real estate assets that exceed €1.3 million for residents. Non-residents can also fall within its scope if they own French property valued above this threshold.

Norway’s wealth tax is an example of how these sorts of levies can lead to unintended consequences.

In 2023, the Norwegian government increased its wealth tax rate from 0.95% to 1% for those with assets between Nkr1.7m (£125,000) and Nkr20m (£1.46 million). This move reportedly resulted in several wealthy people relocating to avoid the tax.

A financial planner could help you stay abreast of any tax changes

If a wealth tax were introduced in the UK, it could have considerable effects depending on how the rules are structured.

If your estate includes high-value property, significant investment portfolios, or a business, you might find that more of your wealth is subject to the new tax.

This could lead to difficulties if you’re “asset rich, cash poor”, as you may struggle to fund these additional payments without selling your assets.

Even if a full-scale wealth tax doesn’t end up materialising, changes to existing taxes could still have a significant effect on your long-term financial security.

For example, the government may decide to align Capital Gains Tax more closely with Income Tax or reduce allowances, which would require careful planning.

This is where you could benefit by working with a financial planner.

While it’s almost impossible to predict how tax legislation in the UK could change, we could help you stay abreast of any potential developments.

We can also explain their meaning for your unique circumstances and offer guidance if things change.

Indeed, we could help you make the most of available allowances to reduce a potential tax bill, or restructure your estate in a way that mitigates Inheritance Tax.

To find out more, please contact us by email at info@investmentsense.co.uk or call 0115 933 8433.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.