The State Pension triple lock was introduced by the coalition Government back in 2010. It was intended to help pensioners who had been suffering under the previous system – a State Pension that rose in line with the Retail Prices Index (RPI), often lower than annual rises in earnings.

The State Pension triple lock was introduced by the coalition Government back in 2010. It was intended to help pensioners who had been suffering under the previous system – a State Pension that rose in line with the Retail Prices Index (RPI), often lower than annual rises in earnings.

It was a 2019 Conservative Party manifesto promise to keep it in place. That, though, was before the coronavirus pandemic.

Recent estimates suggest that the crisis could cost the government more than £300 billion this tax year. Borrowing is at a record high and as the lockdown eases, and the economy begins to recover, the borrowed money will need to be clawed back from somewhere.

Could the triple lock be about to change?

What is the State Pension triple lock?

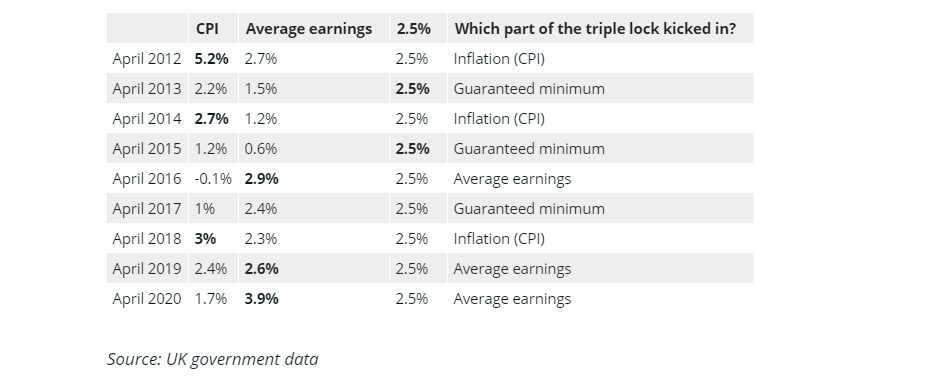

The pension triple lock guarantees that the New and Basic State Pension will increase each year by the highest of:

- 2.5%

- Average earnings growth

- Annual price inflation, as measured by the Consumer Prices Index (CPI)

Since the 2012/13 tax year, two-thirds of the annual increases have been higher than 2.5% – the highest coming in 2012/13 when price inflation (and therefore the increase in State Pension) hit 5.2%.

The triple lock, by guaranteeing a pension increase based on the highest of the above three categories, helps to guard against the State Pension losing value in real terms.

As the cost of living increases, a static pension amount would become increasingly difficult to live on, especially when you remember that retirement income is intended to last for the rest of your life.

With life expectancies rising, that could mean 30 years or more with a pension whose value diminishes as you get older.

As a result, the triple lock guarantee is important for pensioners – and their advisers – when planning retirement.

Why might it be amended or scrapped?

The triple lock is an important guarantee, but it is also an expensive one.

Although it was a manifesto pledge as recently as last December’s General Election, keeping that promise in the face of the coronavirus pandemic and the large levels of government borrowing that occurred as a result, might be tricky.

At the time of the March 2020 Budget, the Department for Work and Pensions forecast State Pension expenditure in 2020/21 of £101.7 billion.

A recent House of Commons Briefing estimated this was £5.6 billion (5.5%) more than if the State Pension had increased in line with earnings since 2011/12, and £1.2 billion (1.2%) more than if the triple lock had instead been a ‘double lock’ – scrapping the 2.5% minimum increase – since 2011/12.

The government needs to recoup some of its expenditure and there are clearly savings to be had by making amendments to the current system.

Back in 2018, a Treasury committee report into household finances, suggested that the triple lock was ‘unsustainable’.

Along with curbs in spending and increased taxes, it seems highly likely the triple lock will be on the agenda when the Chancellor begins to look at where the UK economy is headed post-Covid-19.

What would it mean for my long-term financial plans?

Your retirement income won’t be comprised solely of your State Pension. But at £175.20 per week (or £9,110.40 a year) it does provide a base on which to build the rest of your retirement.

Your pension income, whether it’s made up of private pensions, investments, or regular income from Buy to Let properties, needs to last for the rest of your life. That means keeping up with inflation.

Currently, the pensions triple lock is ensuring the State Pension doesn’t lose value in real terms, but it isn’t guaranteed. The Autumn Budget could see changes so you must be confident and sure of the income you have in place now.

We can help you consider your finances as a whole, building a plan based on all of your income streams and your plans for the future.

It’s impossible to say for certain what changes will be made to help recoup the UK’s coronavirus borrowing.

If the triple lock were to change though – becoming, for example, a ‘double lock’ – you could see State Pension increases diminish in the future and you’ll need a financial plan in place that can absorb that loss.

Get in touch

If you’d like to discuss any aspect of your retirement plans, future financial goals, or how a change to the current State Pension triple lock could impact you get in touch. Please email info@investmentsense.co.uk or call 0115 933 8433.